When starting a new business, there’s a lot to consider, including deciding on the legal structure of the company. A common question business owners ask is, “Should I set up a sole trader or limited company?” Both carry advantages and disadvantages, but what might be right for one business might not be best for you.

This blog explores the differences between both legal structures, giving you the information you need to make an informed decision.

Sole trader vs limited company: what’s the difference?

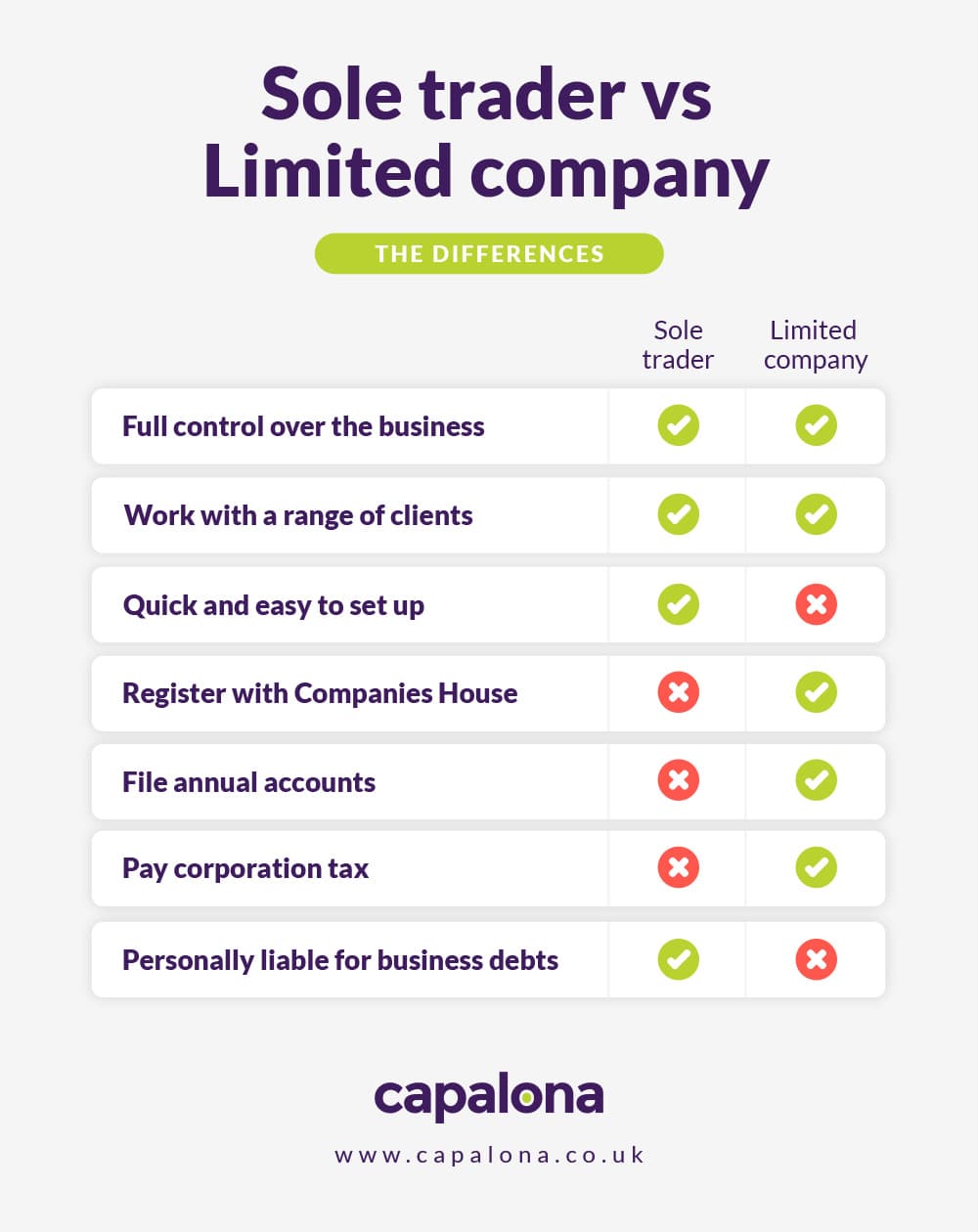

As a sole trader, you are your company; this means you are personally responsible for the business’s profits, losses, and liabilities. However, with minimal admin work and financial privacy, sole tradership is a popular choice amongst startup businesses.

A limited company, however, is a separate legal entity. This means it's completely detached from the owners or directors, providing them with ‘limited liability’; therefore, they’re not personally responsible for the company’s debts and losses. Although a slightly more involved process, many people choose to set up a limited company to benefit from tax efficiencies and a more professional image.

Sole trader vs limited company pros and cons

There are many advantages to becoming a sole trader

First, it’s easy to set up. Simply register your company for an HMRC self-assessment tax return, choose a business name, and you’re done!

As a sole trader, you get to keep your finances private, too — this is because you don’t need to register with Companies House, so you don’t have to declare your accounts and personal details.

And, lastly, there’s minimal legal admin. Simply file one self-assessment tax return each year. To do this accurately, keep track of your sales and expenses through your bank account or accounting software.

Now for the cons… As a sole trader, you might have limited funding options available to you. That’s because some lenders will only lend to limited companies. But even though options might be a little more limited, there are still plenty of loan options, like applying for a sole trader loan.

Some customers or clients prefer to work with limited companies, so being a sole trader might be disadvantageous in some situations, such as winning big contracts. To lessen the risk and become more professional, make sure you have adequate business insurance for your sole tradership.

Unfortunately, as a sole trader, you’re personally liable for company debts. This means if your business can’t repay the debt, the lender will turn to you personally to settle it instead.

How about becoming a limited company?

The most common advantage of becoming a limited company is the tax-efficiency. Where sole traders pay 20-45% income tax (depending on their income), limited companies pay 19% on profits under £50k and 25% on profits over £250k. Limited company directors can pay themselves dividends from the company’s profits, which are taxed at 8.75% (basic rate).

Your personal assets are also protected as a limited company because your business and personal finances are completely separate. You might have more funding options, meaning you can choose from a wide range of business loans, including a limited company loan, or sell shares to investors to grow your company quickly.

And the cons… Setting up a limited company is more costly and complex than a sole trader. There’s more paperwork, including corporation tax, company tax return and profit and loss statement. These complexities might mean hiring an accountant, which can eat into your profits.

As a limited company, your accounts are public knowledge. So your company’s location, finances and performance on Companies House can be viewed by anyone.

Also, remember that you’ll have to abide by company name restrictions when registering your limited company. Check the company name availability checker to see if your chosen name is available and unique before paying money out on branding and product design for a name that you can’t register.

Which legal structure is best for my business?

Choosing a legal structure for your business can be confusing, but even if you change your mind later, you can easily convert your company from a sole trader to a limited company.

If you're currently a limited company, you can also revert back to a sole trader, but this involves a bit more work, including making your limited company dormant or closing it completely.

When choosing your legal structure, you should ask yourself, “How much personal liability am I willing to take on?” If the answer is ‘none,’ then setting up as a limited company could be the better option.

If, however, your small business is low-risk and not in immediate need of investment, setting up as a sole trader could be more suitable.

It’s worth noting that you can’t set up a limited company if you’ve been declared bankrupt or you have a disqualified director order.

How to register your business

Registering your business is relatively straightforward; simply follow the prompts on the HMRC website.

- To register as a sole trader… it’s completely free! Armed with your business name, personal contact details and the nature of your business, you can register for self-assessment within a matter of minutes.

- To register as a limited company… you’ll be £12 out of pocket (£40 if applying by post). After checking if your business name is available, there are a few steps you need to take to register your limited company. Steps include appointing a director, preparing a memorandum, registering for corporation tax and registering for PAYE if you’re paying salaries. Your company will usually be registered within 24 hours, and you’ll receive your certificate of incorporation in the post.

If the thought of registering your business is overwhelming, you can instruct your accountant to register it on your behalf. You can also choose to use your accountant’s offices as your registered business address to keep your personal details confidential (particularly if you’re working from home).

Whether you’re a sole trader or a limited company, applying for a business loan can help you grow faster. At Capalona, we help SMEs find and compare their business funding options in seconds with our free loan comparison tool. Compare business loans.