Recovery Loan Scheme (RLS)

The Government’s business Recovery Loan Scheme (RLS) ended on the 30th June 2024. It provided funding from £1,000 up to £2 million for UK businesses. Here’s everything you need to know.

- Funding from £1,000 to £10 million

- Decisions in as little as 1 hour

- Compare funding options from trusted lenders

- Check your eligibility in minutes

It's fast, free and won't affect your credit score

Trusted by Hundreds of Business Owners

- What was the Recovery Loan Scheme?

- How did the Recovery Loan Scheme work?

- What type of finance was available with the Recovery Loan Scheme?

- What businesses qualified for the Recovery Loan Scheme?

- How did you apply for the Recovery Loan Scheme?

- Did you need to provide a personal guarantee to get a Recovery Loan?

- Did you have to pass a credit check to get a Recovery Loan?

- What was the interest rate on the Recovery Loan Scheme

- Could you qualify for the Recovery Loan Scheme if my business had bad credit?

- Could sole traders apply for the recovery loan scheme?

- CBILS vs Recovery Loan Scheme (RLS) comparison - What’s the difference?

- Recovery Loan Scheme accredited Lenders

- When did the Recovery Loan Scheme end?

- Why use Capalona?

- Recovery Loan Scheme FAQs

What was the Recovery Loan Scheme?

The Recovery Loan Scheme (RLS) launched in April 2021 and supported UK businesses in the aftermath of the pandemic. It replaced all other COVID-related schemes, including the Bounce Back Loan Scheme (BBLS) and Coronavirus Business Interruption Loan Scheme (CBILS).

If you’ve already borrowed money through other Schemes like the ones mentioned above, you can still apply for finance through the new Recovery Loan Scheme, but this might limit the amount you can borrow under the new Scheme.

There is no limit to what you can do with the funding, as long as it’s business-related. Use the Scheme to pay staff wages, re-balance your cash flow, or invest in new markets.

While the recovery loan scheme success rate is not publicly disclosed, the scheme aimed to improve loan terms for businesses, with the government providing a 70% guarantee to encourage lending.

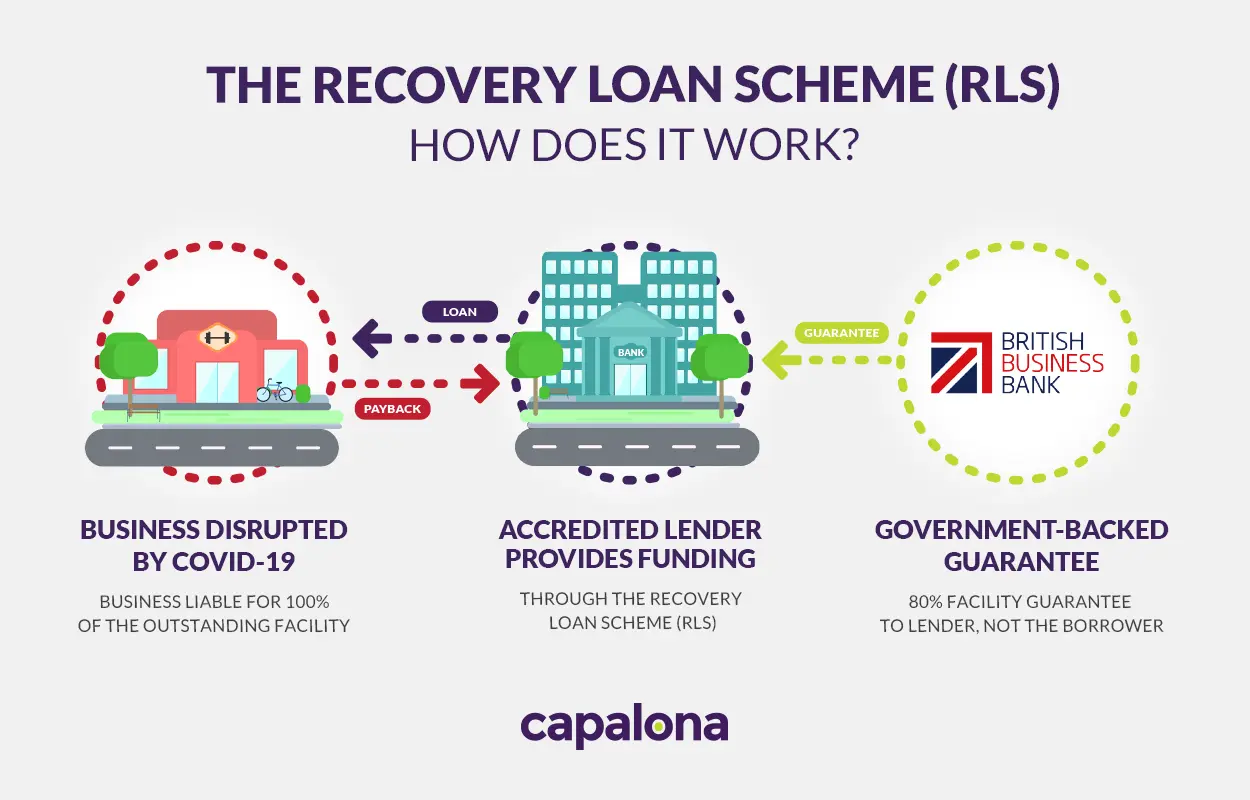

How did the Recovery Loan Scheme work?

The Recovery Loan Scheme aims to improve the terms on offer to your business. That means, if the lender you choose can offer you a different loan product with better terms, they should as they do not require the Government-backed guarantee. The Government-backed guarantee is put against the outstanding balance of the finance and is solely to encourage lenders to lend — they will only guarantee 70% of the Recovery Loan.

Only lenders accredited by the British Business Bank will be able to offer the Recovery Loan Scheme.

And remember - as the borrower, you are 100% liable for debt repayment.

What type of finance was available with the Recovery Loan Scheme?

The types of funding available to your business through the Recovery Loan Scheme (RLS) were as follows:

- Term Loans - from £25,001 up to £2 million per business

- Overdraft - from £25,001 up to £2 million per business

- Invoice Finance - from £1,000 up to £2 million per business

- Asset Finance - from £1,000 up to £2 million per business

What businesses qualified for the Recovery Loan Scheme?

You might be asking yourself “am I eligible for the Recovery Loan Scheme?” We’ve compiled brief eligibility criteria below to help you understand if your business was eligible to apply.

You were eligible if your business:

- Available to businesses with a turnover of up to £45m

- UK based business and must be generating more than 50% of its income from trading activity

- Has a viable business proposition – your lender may disregard (at its discretion) any concerns over short-term to medium-term business performance due to the uncertainty and impact of COVID-19

You would not be eligible if your business:

- Is in ‘collective insolvency proceedings’

- Is a Bank, building society, insurer or reinsurer (excluding insurance brokers)

- Is a public-sector body

- Is a state-funded primary or secondary school

If your business was affected by the coronavirus outbreak and you’re after some additional funding to help your business stay afloat, but you don’t meet the eligibility criteria above, don’t worry. We can help you find an alternative financial solution, it's what we do.

Read more about our alternative financial products.

How did you apply for the Recovery Loan Scheme?

Applying for the Recovery Loan Scheme was straightforward. You could apply directly with an accredited Lender, or use a broker to help you. Along with your application, you would need to provide the following details:

- Management accounts

- Business plan

- Historic accounts

- Details of assets

Did you need to provide a personal guarantee to get a Recovery Loan?

Personal guarantees were taken at lenders discretion, in line with their normal commercial lending practices. If a personal guarantee is taken, the following will apply:

- The maximum amount that can be covered under the Recovery Loan Scheme was capped at a maximum of 20% of the outstanding balance after the proceeds of business assets have been applied.

- No personal guarantees could be held over Principal Private Residences.

Did you have to pass a credit check to get a Recovery Loan?

Just like with every financial application, lenders would perform a credit check. And, as you can imagine, lenders had to carry out fraud checks, too — these loans are for businesses that have been affected by the pandemic and no one else. They needed to ensure the loans are going to those who need them.

What was the interest rate on the Recovery Loan Scheme

Although the government paid the interest for the first 12 months with other coronavirus business support schemes, this was not the case with the Recovery Loan Scheme. You had to pay interest and fees (if applicable) from the beginning. Recovery loan scheme interest rates were capped at 14.99% per annum.

Unlike previous COVID schemes, there was no delay for loan repayment. The first repayment would depend on the lender’s policies, it might have been a month after taking out the loan, or some lenders could offer a Capital Repayment Holiday (CRH). This is something you’ll have to ask your chosen lender.

Could you qualify for the Recovery Loan Scheme if my business had bad credit?

If you have bad credit, this may restrict the finance options available to you and also the interest rate you could secure.

If you’ve been refused credit in the past, you might still have been able to apply for the Scheme. Each lender reviewed each application on a case-by-case basis.

Make sure you explore all the financial options available to your business, check out our business loans for bad credit.

Could sole traders apply for the recovery loan scheme?

Yes, if you’re a sole trader you could have applied for the government-backed Recovery Loan Scheme. You could also apply for the Scheme if you’re a limited partnership, LLP, co-operatives and community benefit societies and corporations.

Alternatively, you can apply for a sole trader loan.

CBILS vs Recovery Loan Scheme (RLS) comparison - What’s the difference?

The biggest difference is that the UK Government isn't covering any loan costs for the Recovery Loan Scheme as they did with CBILS. The original Recovery Loan Scheme offered higher loan amounts (up to £10 million) compared the CBILS and the new RLS. The new RLS loans are available to a wider range of businesses.

All Schemes have the same loan term period of up to six years. So the two big differences are that the amount you can borrow has decreased and the Government won’t pay the interest on your behalf for the first 12 months, nor will they pay an upfront fee on your behalf.

See our table below to compare the differences between the Coronavirus Business Interruption Loan Scheme (CBILS) and the Recovery Loan Scheme (RLS):

| CBILS | RLS | New RLS | |

|---|---|---|---|

| Loan Amount | £50,000 to £5 million | £1,000 to £10 million | £1,000 to £2 million |

| Term | Up to 6 years | Up to 6 years | Up to 6 years |

| Government pays first 12 months interest | Yes | No | No |

| Government pays upfront lender fees | Yes | No | No |

| Government Lender Guarantee | 80% | 70% | 70% |

| Personal Guarantee | No PG's on loans up to £250,000 | No PG's on loans up to £250,000 | PG's may be required, at a lender's discretion |

| Minimum trading history | 1 to 2 years | No minimum | No minimum |

| Minimum annual turnover | No minimum | No minimum | No minimum |

| Closing date | 31 March 2021 | 30 June 2022 | 30 June 2024 |

Recovery Loan Scheme accredited Lenders

The Recovery Loan Scheme (RLS) is managed by the British Business Bank and was only available through accredited lenders. There were 8 lenders accredited for the new iteration of the recovery loan scheme (RLS) so far - here's a list of the lenders:

- Atom Bank

- Bank of Scotland

- BCRS Business Loans

- CWRT

- DSL Business Finance

- First Enterprise

- Genesis Asset Finance

- HSBC UK

- Lloyds Bank

- Natwest

- Royal Bank of Scotland (RBS)

- Ulster Bank

When did the Recovery Loan Scheme end?

The Recovery Loan Scheme (RLS) ended on the 30th June 2024 and was replaced by the Growth Guarantee Scheme (GGS).

Why use Capalona?

Throughout coronavirus, we’ve strived to help as many businesses as possible find the right funding to tide them over this volatile economic period.

At Capalona, we work alongside a range of trusted UK lenders - our sole aim is to find you compare financial products to help your business grow and thrive.

As a broker, our service is completely free for you to use.

Recovery Loan Scheme FAQs

No, this scheme closed in June 2024, so applications are no longer accepted. There’s a new scheme that has replaced it called the Growth Guarantee Scheme. You can access funding through this instead.

Yes, applications were open for sole traders, limited companies, limited liability partnerships, and other types of companies.

Yes, the government provided accredited lenders with a 70% guarantee on loans through the scheme. But the borrower was liable to repay 100% of the loan.

About the author

Adrian T![]()

5/5

Amazingly fast, efficient service, minimal paperwork. So much faster than my business bank of twelve years.