Guarantor Business Loans

If you can’t secure finance by yourself, a great option is to get a guarantor to co-sign. Learn more and apply for a guarantor business loan below.

- Compare a wide range of lenders and rates

- Check your eligibility in minutes

- Find out how much you could borrow

It's fast, free and won't affect your credit score

- What is a guarantor business loan?

- Who can be my guarantor?

- Why would I need a guarantor business loan?

- Business loan guarantor requirements

- Types of business loans with a guarantor

- Alternatives to a guarantor loan

- How to apply for a guarantor loan

Checking won’t affect your credit score

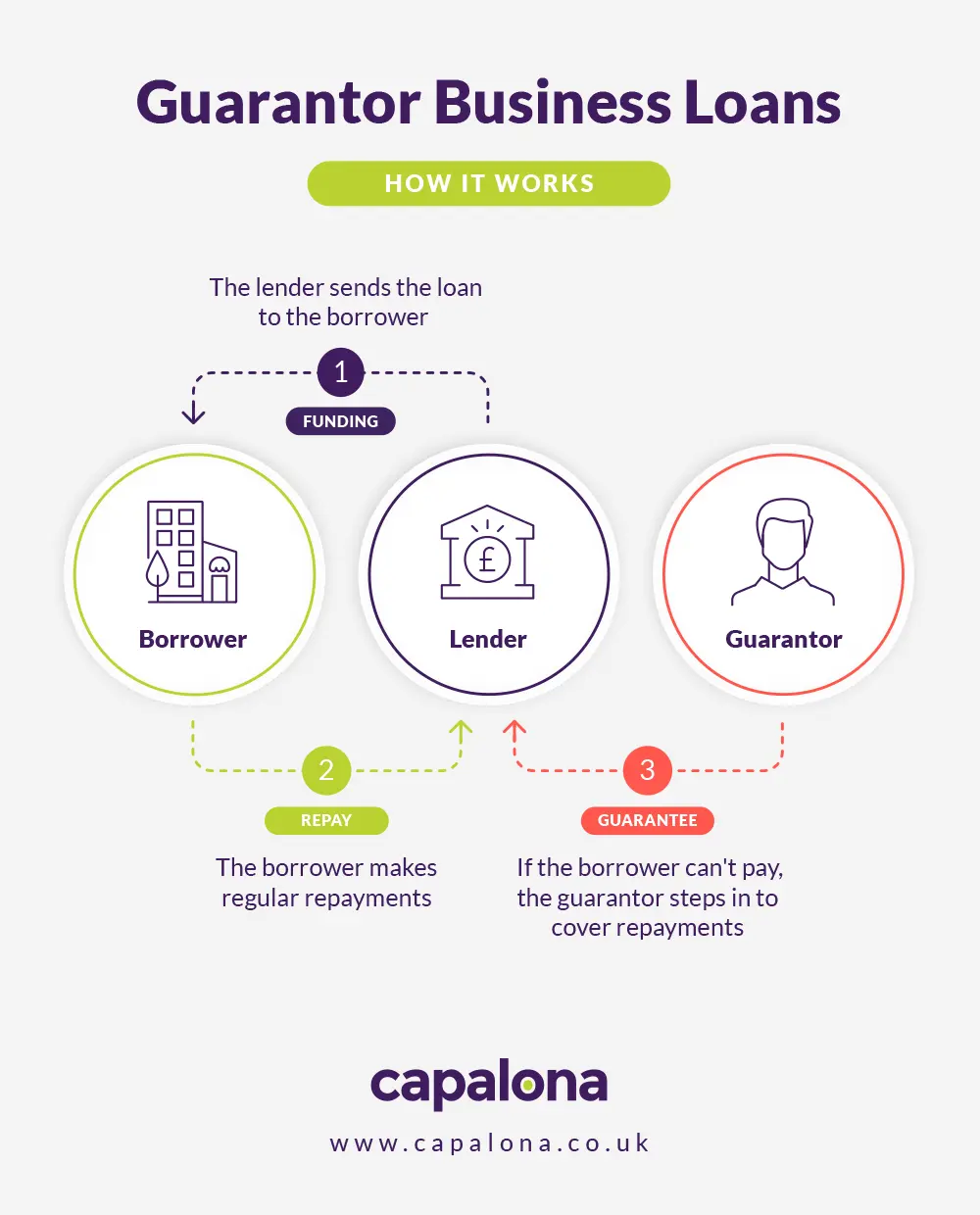

What is a guarantor business loan?

A guarantor business loan is where you get someone else with a good credit score to co-sign for the loan. Should you default on loan repayments, your guarantor is legally bound to repay it on your behalf (they sign a personal guarantee). So, if you’ve got poor credit history, or your business is brand new, the lender might suggest you apply for a guarantor loan.

Who can be my guarantor?

Your guarantor needs to have a good credit history, first and foremost, and many lenders like the guarantor to own a home and be aged over 21. The guarantor usually has a close relationship with the business, i.e. a director or shareholder, but they can also be a close long-term friend or a family member.

Alternatively, you can be the guarantor if you’re the business director and you’re co-signing on behalf of the business entity. I.e. if the business cannot repay, you would repay instead.

Why would I need a guarantor business loan?

There are a few reasons you might consider a guarantor business loan:

- If your business is new or has a limited credit history.

- If you have bad credit as a business owner.

- Getting a guarantor to co-sign mitigates lender risk and helps you access finance you would not otherwise have been able to.

- It helps you access more favourable rates and large loan amounts.

- Means you don’t need to put up business assets as security (particularly if you don’t have any!)

Checking won’t affect your credit score

Business loan guarantor requirements

It’s important to note that every lender has different requirements. For example, most lenders like the guarantor to be a homeowner. But some will be happy if they can provide sufficient evidence that they have enough income or other assets to cover the debt.

Here are some more guarantor requirements:

- Over the age of 21 (some lenders accept guarantors over the age of 18)

- Good credit history

- UK resident

- Family member, a long-term relationship with the borrower, or director/shareholder of the business

Types of business loans with a guarantor

Unsecured business loans

Unsecured business loans carry a higher risk than secured loans. Unsecured loans don’t require collateral, so if you fail to repay the loan, the lender doesn’t have any recourse against you. That’s why they might ask you or another person to sign a personal guarantee, becoming a guarantor.

Large secured business loans

Some secured business loans don’t require a personal guarantee, but if you apply for a large loan, the lender may still ask for extra security in the form of a guarantor. If avoiding this commitment is important to you, there are other finance options that don’t require a personal guarantee available.

Other loan types

There are all kinds of business finance that could require a personal guarantee, including invoice finance and asset finance. Whether you need to sign a personal guarantee will depend on the lender’s specific requirements and how risky a borrower they deem you to be.

Alternatives to a guarantor loan

If you don’t have a suitable guarantor or you don’t think this type of finance is for you, there are plenty of options.

Bad credit business loan

If the whole reason you were considering a guarantor is because of bad credit, you can always apply for a bad credit business loan. Although you’ll have fewer lenders to choose from and higher interest rates to pay, it’s still an option for you if you need to access business finance.

Small Secured business loan

With a smaller-sized secured loan, the lender isn’t as fussed about credit scores as they are for other loan types. That’s because you secure the loan with a high-value asset. If you failed to make timely loan repayments, the lender would seize the asset and sell it on to recoup lost funds. So, although you don’t need a good credit score, you do need a high-value commercial asset, like a property or vehicle.

Checking won’t affect your credit score

Invoice finance

Invoice finance is perfect for those looking for an alternative to guarantor loans. You simply sell one or multiple outstanding invoices to the lender, who then advances you up to 95% of the unpaid invoice value. When the customer pays, they deduct their fees and transfer the outstanding balance to you.

As the invoice is taken as collateral, they’re not interested in how long your business has been running for or whether you have good credit. The lender will want to buy invoices from reputable customers; however, as long as you work with creditworthy customers, you could be eligible to apply for invoice financing.

Merchant cash advance

A merchant cash advance is simply an advance on your future sales. Repaid as a percentage, this type of finance doesn’t require solid credit to access. Instead, your business’s sales are the important thing in this agreement. The more revenue via card sales you make, the better your chances of qualifying for a merchant cash advance.

How to apply for a guarantor loan

Applying for guarantor business finance is quick and easy. To start, use our free loan comparison tool to find and compare the best guarantor small business loan options for your specific business needs. Compare total repayable, interest rates, average monthly repayments, and more.

After you find a suitable loan, you can click through from the loan offer and continue with your application with the lender.

Ready to get started? Find and compare guarantor loans here. (Getting a quote won’t affect your credit score.)

About the author

Adrian T![]()

5/5

Amazingly fast, efficient service, minimal paperwork. So much faster than my business bank of twelve years.