You’ve probably heard the terms hard credit check and soft credit check, particularly if you’re looking to access business finance, but what do they mean? And what’s the difference between the two?

Understanding the difference between the two terms can help you avoid accidentally damaging your credit score.

This blog explains the differences, how they affect your business, and what they mean when you’re applying for a business loan.

Key Takeaways

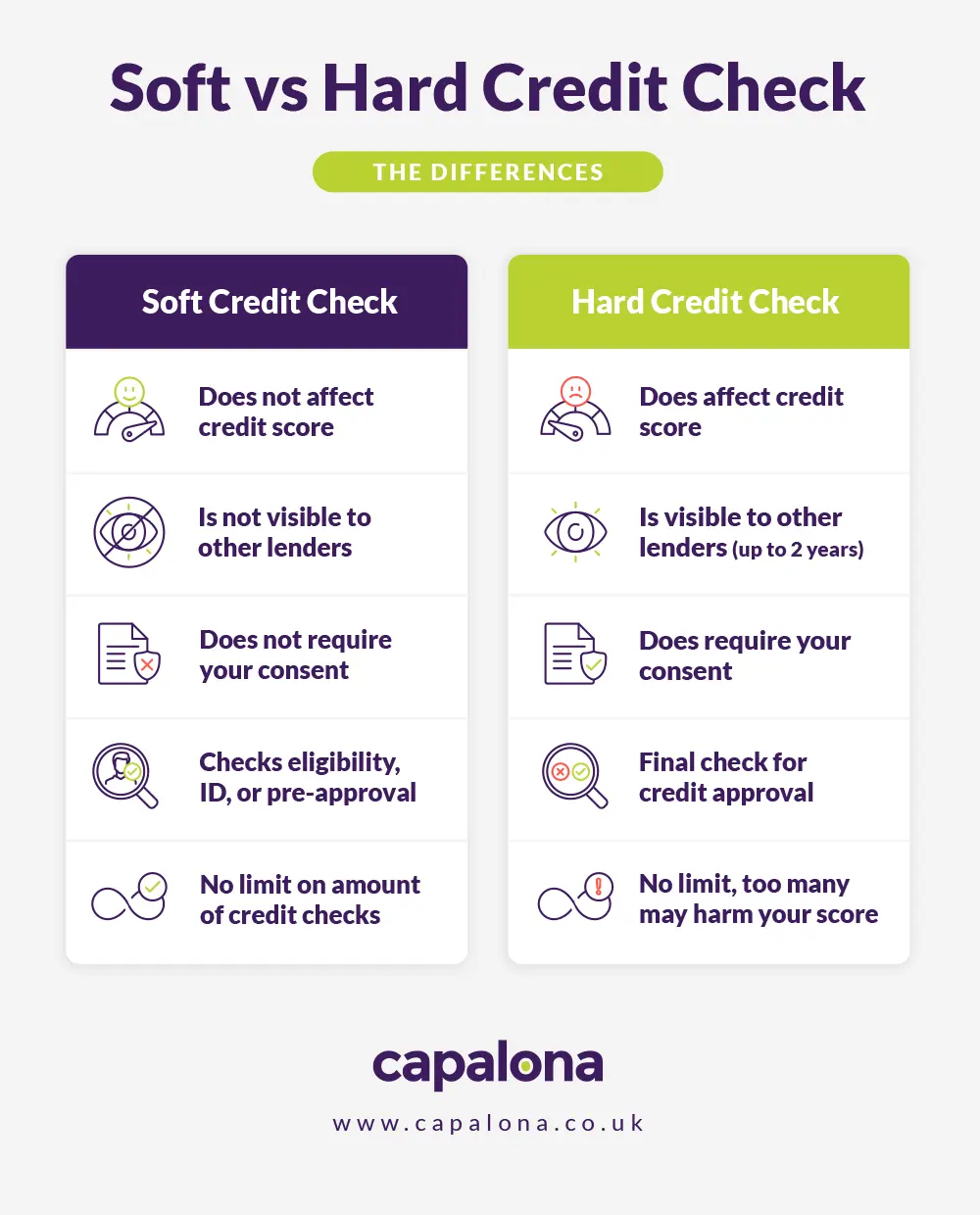

- A soft credit search gives lenders a snapshot of your credit profile. All without leaving a mark on your profile, so other lenders can see it. This means it won’t affect your credit score.

- A hard credit search is a deep dive into your credit history. This leaves a mark on your credit file which is visible to other lenders. And having too many of these searches performed in a short period of time can lower your credit score.

- By using an eligibility checker that runs only a soft search first, like Capalona’s free business loan comparison tool, you can explore your eligible funding options without impacting your credit profile.

What is a hard credit check?

A hard credit check is a comprehensive review of your credit file. So, every time you apply for credit, i.e., a small business loan, mortgage, credit card, or mobile phone contract, the lender requests a full copy of your credit report from one of the UK’s credit reference agencies (Experian, Equifax, or TransUnion).

This report shows the lender your borrowing history, any missed payments or defaults, outstanding debts, or County Court Judgements (CCJs).

When does a hard credit check happen?

Lenders perform hard credit checks when you make a formal application for credit. Here are some examples:

- Applying for a business loan or personal loan

- Applying for an overdraft of credit card

- Taking out a mortgage

- Taking out a pay-monthly phone contract

- Taking out car finance

Does a hard credit check affect your credit score?

A hard credit check can affect your credit score by temporarily lowering it. Particularly, if you’ve made several credit applications in a short period of time.

If a lender sees multiple hard searches on your credit file, it can indicate to them that you’re financially struggling and urgently seeking credit. All these signs might lead the lender to flag you as a high-risk borrower. This can reduce your chances of loan approval and affect the interest rates you’re offered.

What is a soft credit check?

A soft credit check is a more surface-level look at your credit file. These checks give the lender basic information about your creditworthiness. A soft search doesn’t leave a visible mark on your credit file.

You can see all soft searches on your own credit report, but no one else can. This means it can’t affect your credit score, regardless of how many times they’re carried out. A soft search gives you a great opportunity to compare business finance options before proceeding with a full loan application.

When does a soft credit check happen?

They’re pretty common in the following situations:

- When you check your own credit report

- Using an eligibility checker through a comparison site (like Capalona)

- Getting pre-approval from lenders (i.e. for a new credit card)

- When employers carry out identity or background checks

- When an existing lender reviews your account

Soft credit check vs hard credit check

Here’s a quick comparison to help you decipher the main differences between soft and hard credit checks.

| Soft credit check | Hard credit check | |

|---|---|---|

| Visible to other lenders? | No | Yes |

| Affects credit score? | No | Yes, but only temporarily |

| Requires consent? | No | Yes |

| Stays on your credit file? | Yes, but is only visible to you | Yes, for up to two years |

| When does it happen? | Eligibility checks, identity checks, and pre-approval | Formal credit applications (loans, mortgages, credit cards) |

| Limit on how many? | No | No limit, but too many can cause damage to your credit score |

What do soft credit checks show?

Soft searches only give lenders a top-level overview of your financial situation. Therefore, a soft check will only show lenders:

- Your basic details, like name, address, and date of birth

- Any outstanding debts, i.e. loans, mortgages, credit cards

- Any public records, like CCJs or bankruptcies

- An overview of your repayment history, including late or missed payments

Soft search bad credit loans

If you want to access finance to grow your business, but you have a less-than-perfect credit score, you might be worried about what happens when a lender checks your credit file. Which is completely understandable.

But that’s why the soft search is so valuable. Comparing loans using a soft search means you can find out whether the lender will likely approve you for a business loan for bad credit before committing to a full loan application.

The loan application process will only become harder for your business if you apply for several loans, are then rejected, and are left dealing with multiple hard credit checks sitting on your credit report.

It’s important to note that even with bad credit, lenders won’t automatically reject your application. Unlike traditional banks, alternative lenders look past your credit score and consider other factors like your trading history, turnover, and performance before making their lending decision (plus, you can sign a personal guarantee).

How to protect your credit score when applying for business finance

You might have good credit, or you’re hoping to improve your credit score; either way, there are some easy steps you can take to protect it further:

- Always use an eligibility checker before applying. Tools that use soft search, like Capalona, help you understand your eligible options without risking damage to your credit score.

- Spread out your credit applications. Don’t submit multiple credit applications in a short timeframe.

- Check your own credit report regularly. By checking your credit report, you can spot errors that can pull down your score. Checking it regularly won’t affect your score, and it gives you the chance to correct anything before it has any impact.

Hard vs soft credit checks FAQs

Does Capalona run a soft or hard credit check?

As a broker, not a lender, our business loan eligibility checker only carries out a soft credit search. This search helps our tool match you with eligible business finance options.

Does checking my own credit score count as a hard search?

No. When you check your own credit report, it counts as a soft search and can’t impact your credit score.

How many hard searches are too many?

If you’re submitting more than one credit application within a six-month window, this can raise red flags for lenders. Most hard searches fade from your file after 12 months, but can take up to two years, so they won’t be there forever.

Is there such a thing as a no-credit-check business loan?

Financial Conduct Authority (FCA) rules require all regulated UK lenders to carry out responsible lending checks. But the good news is that some lenders offer loans that focus on trading history or turnover rather than credit scores. So even with a poor credit history, there are loan options available to you.

Does being rejected for a loan affect my credit score?

The rejection doesn’t, but the hard search they carry out through the application process does. That’s why it makes sense to use soft search eligibility checkers like Capalona to find eligible loan options before applying.