LATEST Hard asset finance vs soft asset finance Learn the differences between hard asset vs soft asset finance, enabling you to choose the right type of asset financing for your business. Tips & Guides

How to start and successfully run a hotel business Learn how to run a hotel business successfully, with our expert tips on guest experiences, operations & loans. Boost your growth with smart financing. Tips & Guides

What are the different types of VAT? Learn about the 3 types of VAT, including standard rate, reduced rate & zero rate, along with the types of VAT schemes available to you. Tips & Guides

How to ask for upfront payments for your business Learn how to ask for upfront payments in your business confidently with our expert tips and template examples, to ensure smooth transactions. Tips & Guides

Capalona Wins Best Fintech Website / Platform 2025 at Business Awards UK! We’re absolutely thrilled to share that Capalona has been named the Best Fintech Website / Platform 2025 at the Business Awards UK! News

Capalona Shortlisted for 2025 Fintech Awards Capalona is proud to announce that we have been shortlisted for the prestigious '2025 Fintech Awards' at Business Awards UK! News

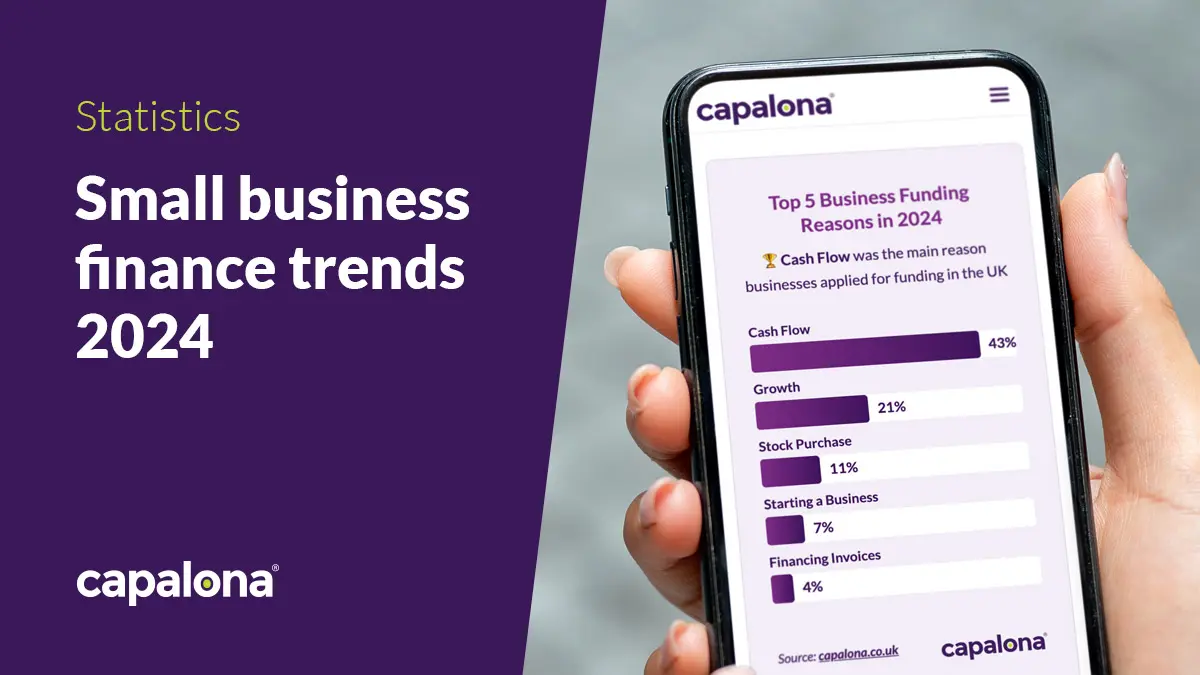

Small business finance trends 2024 We take a look at some interesting statistics in business loans over 2024, including loan amounts and which business types are seeking the most loans. News