If your company is asset-rich but cash-poor, consider using your assets to boost working capital to grow your business.

Assets fall into two categories: hard assets and soft assets. Not sure what the difference is? Don't worry, in this blog, we’ll define both, share examples, and explain how you can use them when applying for business finance.

What are hard assets?

A hard asset is a high-value tangible asset, like a property, that can be used as collateral when applying for a loan.

Lenders prefer these types of assets as they provide a higher level of security because they generally retain their value over time. They're easy for lenders to claim and resell if you default on your loan repayments.

Because a hard asset lowers your borrowing risk to the lender, you can usually get a larger loan with better repayment terms than when you secure a loan with soft assets.

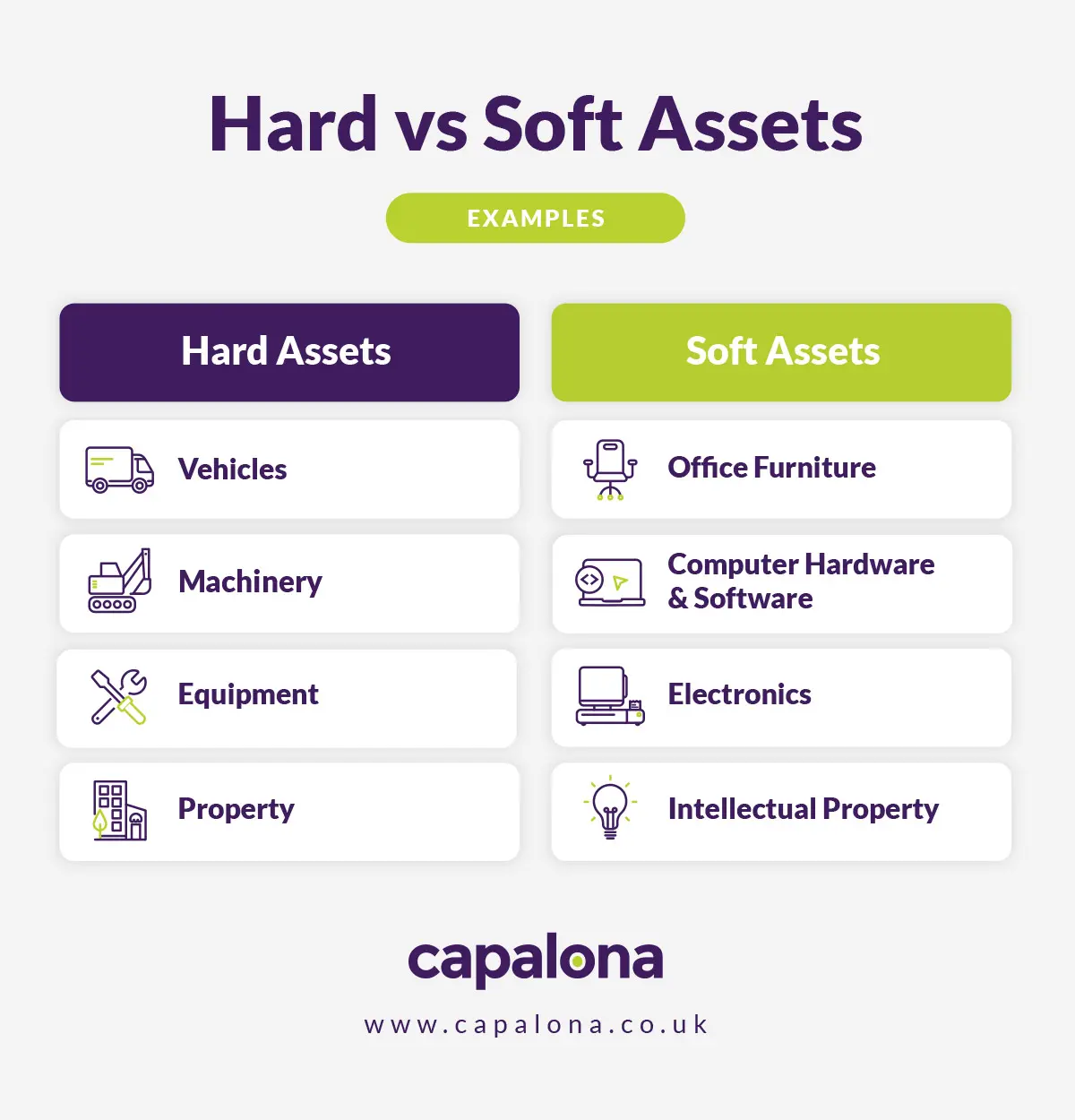

Examples of hard assets

- Vehicles such as cars, trucks, vans, coaches, tractors, etc

- Machinery or plant equipment

- Engineering or manufacturing equipment

- Real estate, both domestic and commercial properties, and any other valuable buildings

- Commodities such as oils, agricultural products, metals, etc

How hard asset financing works

The hard asset acts as collateral to secure the loan. You can use this finance to access cash tied up in an existing asset, or it can be used in a hire purchase agreement or lease agreement for equipment or vehicles. With a hire purchase agreement, you can purchase the asset outright at the end of the term, upgrade the asset, or return the asset if no longer needed.

What are soft assets?

A soft asset, although essential to your business, is less desirable to use as collateral for lenders. This is because a soft asset has very little resale value, and the value it does have depreciates quickly.

Although accepting soft assets as collateral is less common, there are lenders willing to accept them. You might have fewer loan options and less favourable terms and interest rates.

Examples of soft assets

- Office furniture (chairs, desks, filing cabinets)

- Electronic appliances (phones, printers, microwave)

- Computer-based hardware and software

- Intellectual property (eg, patents and trademarks)

- Audio-visual equipment

Methods of financing soft assets

Revenue-based finance. With this type of financing, the lender receives a percentage of your future revenue instead of securing it with a hard asset. So, if your business makes its income from soft assets like software, revenue-based financing could be a good option.

Asset-based financing. Although this type of financing is historically secured with hard assets, some lenders will consider soft assets in asset financing if they’re well documented, i.e. intellectual property that generates revenue.

Soft asset financing. You can hire purchase or lease soft assets through soft asset financing. The asset you’re purchasing or hiring becomes the security for this type of finance. So you can purchase equipment without a significant financial outlay, helping you better manage your finances and improve cash flow.

Difference between hard and soft assets

Although some lenders will accept both hard and soft assets as collateral, there are some big differences between the two.

Tangibility of the asset

Hard assets are tangible, they're physical items such as vehicles, property, and machinery that hold or appreciate in value. While soft assets can be both tangible and intangible, and will generally be less valuable, such as software, office furniture or a patent.

Retention of value

Hard assets tend to be more valuable to start with and will continue to hold their value for longer, or in some cases, they will appreciate in value (like property). Soft assets, on the other hand, have much less value to start with and will almost certainly depreciate in value over time.

Financing ease

Hard assets are very easy to finance as they're strong collateral - if the borrower defaults on the original loan agreement, the lender can easily repossess the asset, resell and recoup their investment. Soft assets, however, are more difficult to finance due to their lower value and, often, intangibility.

Challenges when using soft assets

It’s not just lenders who stand to miss out if you secure finance using soft assets; it’s you (the borrower). Trying to sell soft assets can pose risks and challenges for the lender, i.e. they don’t retain their value as well, so it becomes challenging to recoup lost investments. But, because of this risk, the borrower shoulders higher interest rates, a longer loan approval process, and potentially unfavourable terms.

How to apply for asset-based financing

Applying for asset finance is quick and easy, whether you’re interested in hard asset lending or soft asset financing. First, you can find and compare eligible asset finance options through our free self-serve comparison platform. Simply share what you’re looking for, and our tool will instantly show you eligible products in table form for you to compare like-for-like.

If you find a product you like, you can selectthe lender to continue with your application. The lender will likely ask you for documentation, including proof of ID, proof that you own the asset, an up-to-date valuation showing market value, bank statements and more.