Staying informed about your business finances is crucial; without visibility into your finances, you don’t know how much cash you have. Can you pay your staff? Can you pay your rent and other bills? Ultimately — can you keep your business running?

You shouldn’t have to ask these questions; you should know the answers already.

When it comes to finances, you don’t want any surprises. So keep reading to learn how to calculate working capital and its importance.

What is working capital?

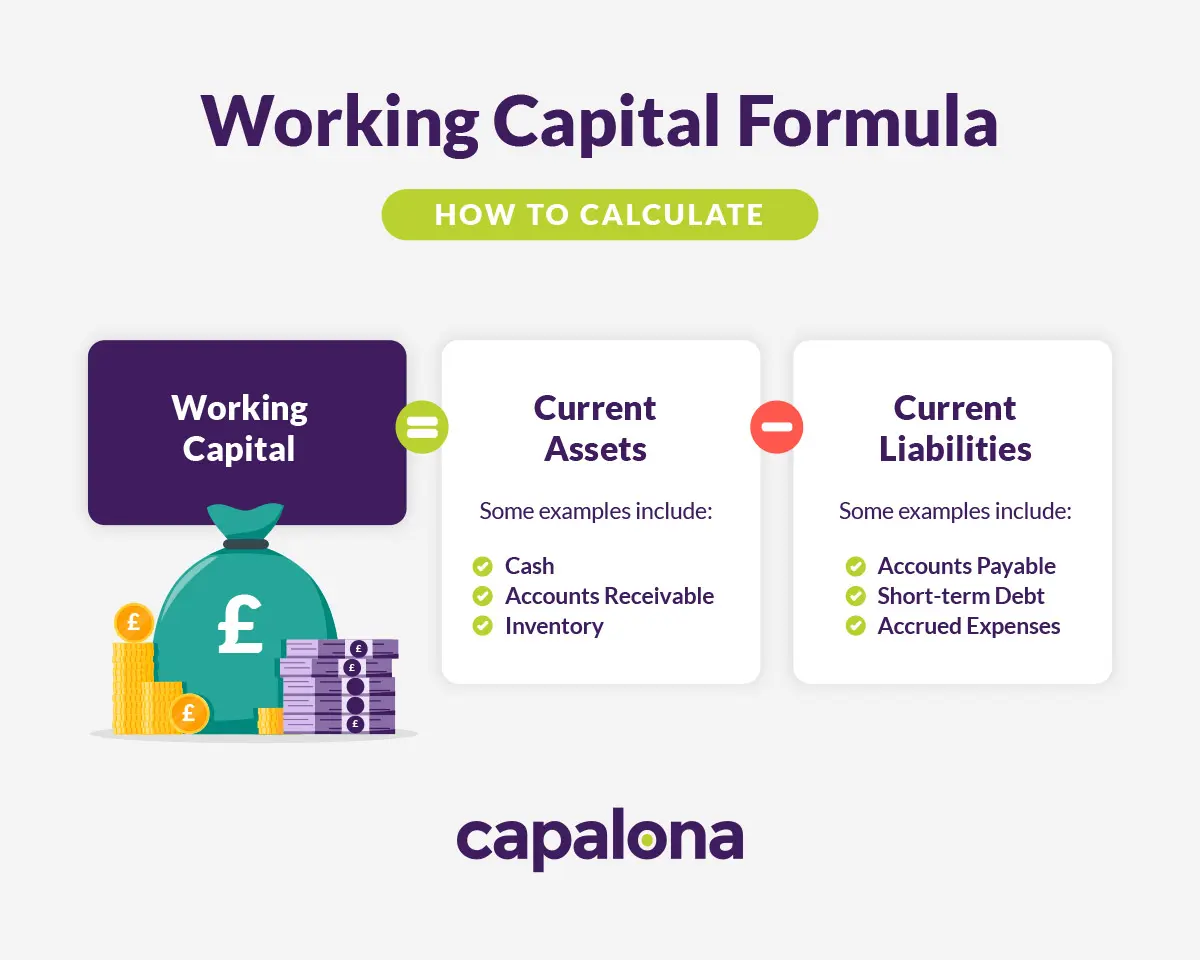

Working capital is the financial health indicator of your business in the short term. You calculate it by subtracting current liabilities from current assets. Effective working capital management means maintaining a healthy cash flow to pay your operating expenses and debts comfortably.

Importance of working capital

Without working capital, you can’t pay your bills, lenders can seize your assets, and you run out of money. So working capital is crucial for your business’s survival, and knowing how to calculate it means you can analyse your finances regularly and stay informed about your business’s financial position, always.

The components of working capital

When understanding working capital, there are two terms you should become familiar with — current assets and current liabilities.

What are current assets?

Current assets are liquid assets that can be converted into cash quickly, i.e. not your other assets like property, vehicles, or land. Your current assets can be broken down into the following three categories:

- Cash — This is cash on hand and cash currently in your business bank account.

- Accounts receivable — This is money customers owe you that you’re awaiting payment on.

- Inventory — The value of the goods you have in your inventory.

What are current liabilities?

Current liabilities are debts your business owes over the next 12 months; these can be broken down into the following three categories:

- Accounts payable — these are supplier invoices you haven’t paid yet.

- Short-term debt — If you have a business loan to repay, include all short-term loan repayments to be made within the year.

- Accrued expenses — these expenses have been incurred but not paid out yet, such as salaries.

Working capital formula

To calculate your net working capital, use the following formula:

Working Capital = Current assets - Current liabilities

An example of working capital

How can calculating working capital look? Here’s a basic example.

| Current Assets | |

| Cash | £15,000 |

| Accounts receivable | £20,000 |

| Inventory | £5,000 |

| £40,000 | |

| Current Liabilities | |

| Accounts payable | £10,000 |

| Short-term debt | £5,000 |

| Accrued expenses | £3,000 |

| £18,000 | |

| Positive working capital: | £22,000 |

What happens if I have negative working capital?

You have negative working capital if your current liabilities are more than your current assets. This means you owe more money than you currently have. In this instance, you should try and increase your liquid assets or decrease your current liabilities.

The best outcome when calculating your working capital is having positive working capital, which means you have stable short-term finances. This means you can pay your business expenses and operate relatively smoothly.

If you have zero working capital, although it’s not the best news, there’s a chance you can still operate efficiently, but if you have to pay out for unexpected bills or cover other expenses, you’ll find yourself in a sticky situation.

5 ways to improve your working capital

If your current liabilities outweigh your current assets or your working capital is at zero, you can do a few things to improve your working capital.

1. Boost your revenue

You can rebalance the scales of assets and liabilities by boosting your revenue. You could boost revenue by increasing your prices, implementing new products or services that don’t increase your expenditure, growing your customer pool, or focusing on retaining existing customers.

2. Downsize your office space

If you can downsize your office space, you could save considerable money on your office lease. Many businesses are now adopting a hybrid working model, saving you up to 50% on office costs. This is a strategy you can consider if your staff can work efficiently from home.

3. Consider business finance

To boost your short-term working capital, you can apply for between £5,000 and £500,000 with an unsecured business loan. These working capital loans are fast and flexible and can be repaid within five years. These loans give you peace of mind, giving you the healthy cash flow you need to keep your day-to-day business operations smooth.

We work with a panel of trustworthy UK lenders; check out all our business finance products.

4. Make redundancies

If you can’t afford to pay your staff, you might have to consider making difficult redundancy decisions. One of the biggest expenses for businesses is payroll. But before you make any hasty decisions, consider how you’ll manage your operations with fewer staff members — you don’t want this decision to disrupt the service your customers receive.

5. Negotiate with suppliers

Negotiate your existing supplier contracts to reduce costs. You should also negotiate with utility providers, i.e. gas and energy suppliers. Utilities can consume a considerable portion of your business expenses; that’s why you should compare business energy providers to ensure you get the best energy deals.

To sum up

To run your business effectively, you need to grasp what working capital is, its importance and how to calculate it accurately. By understanding this financial metric, you’re better able to make informed business decisions, cutting costs where necessary to maintain a positive working capital.

If you want to increase your working capital with a business loan, we can help you find the best loans out there. Use our quick and easy loan comparison tool to compare UK lenders in seconds (it’s free!). Find and compare business finance.