When researching business loans, you might have seen the term ‘factor rate’ with an accompanying figure. If you’re wondering what that figure is and how you can use it when considering loan options, this is the blog for you.

Keep reading to learn more about factor rates, how you calculate them, and what kind of loans use them.

What is a Factor Rate?

A factor rate represents how much you owe for every pound you borrow. The rate is given as a decimal number (i.e. 1.1). This is to help you calculate the total repayment amount. The factor rate formula can be useful when planning your finances to double-check that you can comfortably afford the required loan payments before entering into a loan contract.

Factor rate calculator

You can use the following factor rate formula to calculate your factor rate repayments:

Total Repayment = Advance Amount × Factor Rate

Let’s say you borrow £150,000 as a merchant cash advance. You multiply that by the factor rate, let’s say that’s 1.2. Your total repayable is £180,000. You can factor the extra £30,000 it’s going to cost you over the loan term to see if it’s truly an affordable way to fund your business growth.

£180,000 = £150,000 x 1.2

Factor Rate Calculator

Your results

Total Repayment:

£15,000.00

This calculator is for illustration purposes only. Actual costs may vary depending on lender terms.

Factor rate loans

Some alternative finance providers will offer factor rates instead of interest rates. Here are some products that charge factor rates:

Merchant cash advance

A merchant cash advance is given as a lump sum, like most loans, but you repay this one as a percentage each month instead of fixed monthly payments. The payments are automatically sent to the lender, and how much you can borrow is based on your credit and debit card sales. The factor rate determines the total amount you repay through these daily, weekly, or monthly payments. Although you’ll repay the loan faster if you process more credit or debit card sales, you will still repay the same amount.

Invoice finance

Factor rates differ slightly for invoice finance. With invoice finance, you borrow against unpaid invoices, and, in most cases, the lender can lend you up to 95% of the entire unpaid invoice amount. The lender can charge a flat factor rate fee, which remains fixed, regardless of how long the customer takes to pay the invoice, or they can charge a tiered fee. This fee can fluctuate depending on how long the customer takes to pay.

Short-term business loans

When applying for a short-term business loan, you’re looking to access quick and simple funding for your business. That’s why a factor rate is charged on a short-term loan instead of interest. The fees are easier to understand and quicker for alternative lenders to approve. These loans are usually repaid within 24 months.

What influences a factor rate?

You’ll notice you might receive a different factor rate for different loan products or by lender. That’s because there are a few things that influence the factor rate. A factor rate isn’t the same for everyone; it’s an individual rate based on your financial circumstances, market conditions, and the type of product you apply for.

Here are five factors that can affect your factor rate:

- Revenue consistency. If your revenue streams are predictable and strong, you pose less of a risk to the lender (and by extension, the lender’s money). So you’ll find your factor rate is lower.

- Creditworthiness. The same goes for your credit score. If the lender reviews your business and personal credit score and finds you always pay on time, you never default, and you have a long trading history, you’re all set for a lower factor rate than someone who doesn’t meet those standards.

- Loan amount. If you apply for a large sum of money, this can impact the lender’s factor rate. The higher the sum, the higher the risk.

- Length of loan term. If you’re looking to borrow over a long period of time, let’s say 5-10 years or more, the lender has a greater chance of witnessing market changes over this period, increasing risk to their money.

- No security. Applying for unsecured loans opens the lender up to further risk. But if you apply for secured loans, offering collateral like commercial property, the lender is more likely to offer you a competitive factor rate.

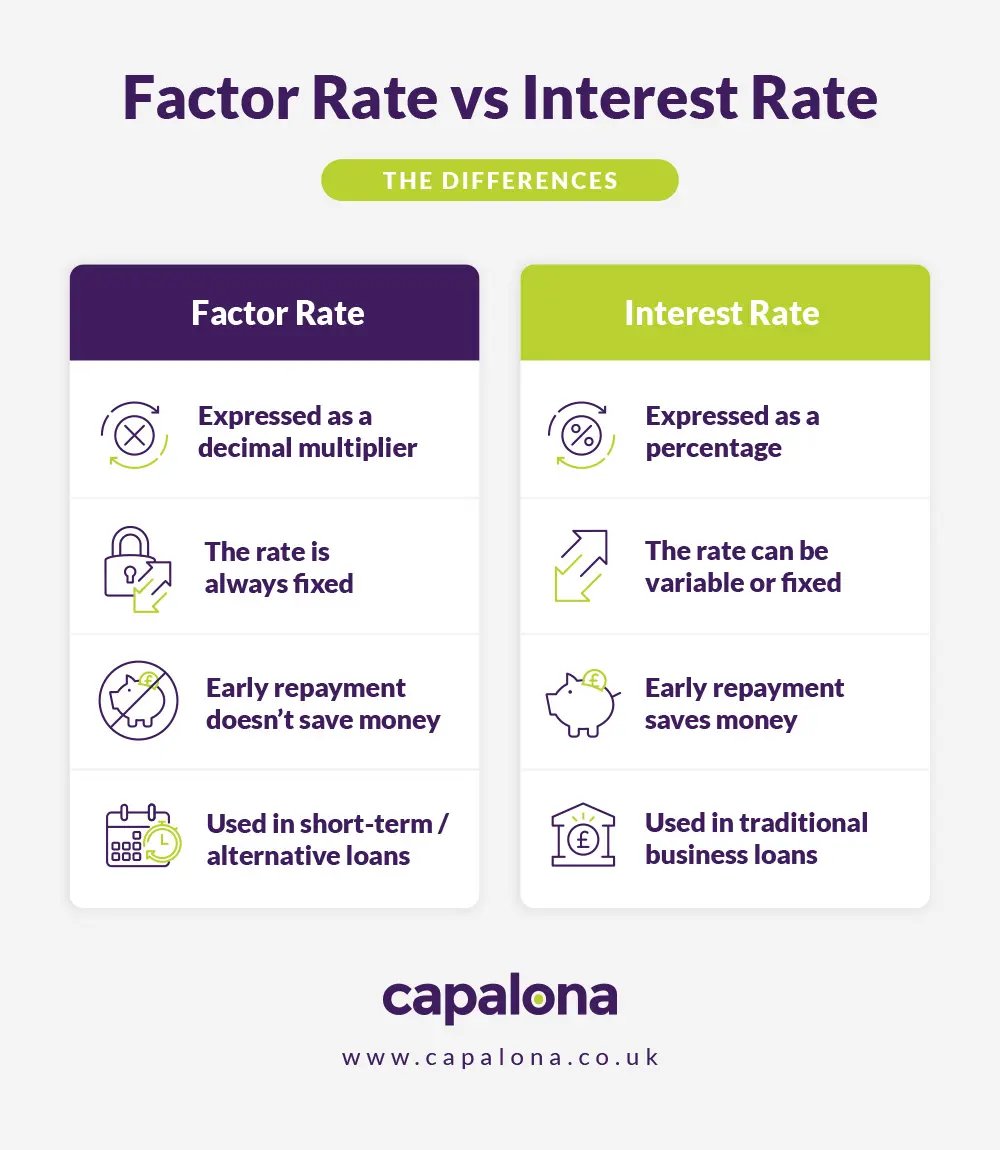

Factor rate vs interest rate

Lenders will not charge a factor rate and an interest rate on the same product. They are both different ways for lenders to charge borrowers for lending.

Interest rates

These rates are expressed as a percentage and can be either fixed or variable, and are typically attached to traditional business loans. Interest accrues, which means the quicker you repay the loan, usually, the cheaper the loan becomes.

Factor rates

A factor rate is fixed and known by the borrower upfront, which makes it easier to understand the entire financial undertaking before completing your loan application. Unlike interest rates, a factor rate remains the same throughout the loan term, which means even if you do repay the loan quickly, you’ll still repay the same amount.

Can you convert a factor rate to an interest rate?

Yes! While a factor rate and an interest rate (or APR) measure borrowing costs differently, you can convert between them to better compare your funding options. Use the calculator below to see how your factor rate translates into an approximate interest rate or APR.

Factor Rate to APR Calculator

Your results

Estimated APR:

50.00%

This calculator is for illustration purposes only. Actual costs may vary depending on lender terms.

Applying for a business loan

If you’re wondering how to get a business loan, getting started is quick and easy. Start by using our free business loan comparison tool to find and compare lots of eligible business loans in one place. Explore the options available, click to expand and read more about each option (our tool includes the factor rates or interest rates for each product).

If you find a loan offer you like, simply click through to continue with your application on the lender’s website.

Getting a quote is free, it will not affect your credit score, and you’re under no obligation to accept any loan offer.