Get the right funding for your business

Everyday we help lots of businesses just like yours get the funding they need. From start-ups to well established companies, we can help your business grow.

- Compare a wide range of lenders and rates

- Check your eligibility in minutes

- Find out how much you could borrow

It's fast, free and won't affect your credit score

A transparent service that leaves you in control

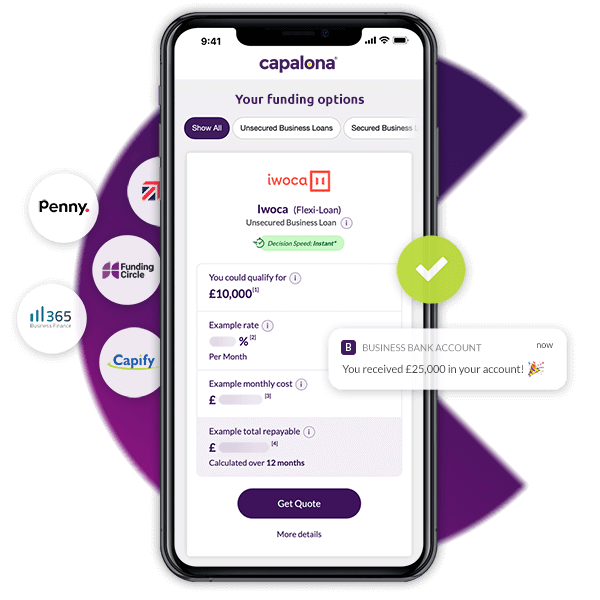

A funding platform that gives you even more control than ever before, displaying business loan matches and a level of detail that puts you in the driving seat.

Fast, fair & transparent

Discover a funding journey that's quick, totally transparent and free from bias.

Easy-to-use comparison

We provide you with the information you need to make an informed desicion with ease.

See how much you could borrow

We show an instant estimate of how much you could borrow for each funding option you are eligible for.

Multiple funding choices

Our panel includes bank and non-bank lenders offering business loans, merchant cash advances, invoice finance and more.

It's free, forever

Capalona is a free-to-use business finance matching platform. We don’t charge a penny!

No credit impact

Using our platform to see your funding options will not affect your credit score.

We compare a panel of trusted UK lenders

We help connect your business to the right providers

Tell us about your business

Start your search for business funding by filling out our secure online form about you, your business and your funding needs.

See your funding options

We'll quickly check your eligibility across multiple business lenders to find you suitable funding options for your business.

Compare and apply

Simply select the lender(s) you would like to apply with, and funding could be with you in just a few hours.*

* Fund speed and transfer times will vary depending on the lender.

Get StartedIt’s fast, free and it won't affect your business’ credit score.

Proud to support British Businesses

Whatever your industry sector, circumstances or credit rating, we've helped many businesses across England, Wales, Scotland and Northern Ireland secure the finance they need to grow.

Adrian T![]()

5/5

Amazingly fast, efficient service, minimal paperwork. So much faster than my business bank of twelve years.

Featured Products

Unsecured Business Loan

Flexible, alternative finance solutions without offering security.

Get StartedMerchant Cash Advance

Raise unsecured finance against your future credit/debit card sales.

Get StartedShort Term Business Loans

Short term business loans can offer the solution you need for your business.

Get StartedCommercial Property Finance

We can find the right property finance option for your business.

Get StartedCan't find the funding solution for your business?

View our full range of funding options here.

More than just finance

Capalona can also help you find the right deals on your business essentials

We’ve funded businesses from all sectors

View more business sectors here.

Tips & Guides

Where to get business money advice

Written by Helen Jackson | April 08, 2024

Knowing where to go for business money help or advice can be confusing, so we’ve put together some guidance on where to look.

How to get a business loan

Written by Helen Jackson | April 08, 2024

Interested in getting a business loan but don’t know where to start? We’ve put together a guide on how to secure a business loan.

How to do a cash flow forecast for your business

Written by Helen Jackson | March 11, 2024

A business cash flow forecast is a plan that shows how much money your business is expected to receive and payout.

What is business risk and how to minimise it

Written by Helen Jackson | March 21, 2024

Business risks are internal and external factors that can affect profit. Understand what business risk is with tips for minimising risk in business.